19 Feb 2026

IT-Service valuation update | Q4 2025

IT-Services multiples have normalized since the 2021 peak (15.9x), with investors now pricing the sector on visibility, profitability and delivery quality rather than pure revenue growth.

Valuations are anchored in the high single- to low double-digit EV/EBITDA range. Premiums accrue to models with higher recurring mix, stronger cash conversion and industry-specific differentiation, while generic capacity-driven models trade at a discount.

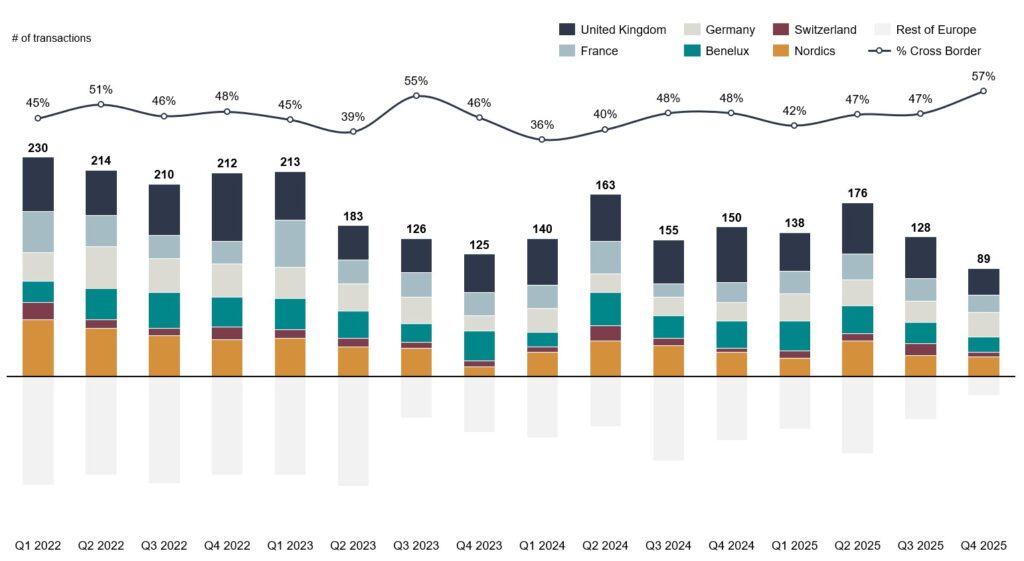

European countries with Investec presence on the ground (UK, France, Germany, Benelux, Switzerland, Nordics) account for >85% of Q4 2025 deals, indicating a high overlap between observed M&A activity and Investec’s geographic footprint.

Cross-border share steadily increasing to 57%, Investec present in all main markets

Except for Q2 2025, deal flow further softened in Q4 2025 as buyers became more selective, focusing on assets that demonstrate repeatable execution at scale, governance, high-quality revenue streams and delivery reliability. Cross-border share rose to 57% in Q4 2025, reflecting a clear shift towards pan-regional delivery and regulatory coverage of country specific requirements.

Key drivers behind the cross-border tilt:

- Regional AI & cloud roll-outs: accelerating AI-driven cloud demand and larger strategic managed services awards are reinforcing multi-market delivery requirements

- Regulation / sovereignty: frameworks like NIS2 raise requirements for supply-chain security and controls, increasing the value of in-market presence and auditable compliance

- Ecosystem consolidation: roll-ups around Microsoft, Salesforce, ServiceNow are being used to standardize delivery and unlock cross-sell across geographies

Outlook 2026: buyers are re-engaging, but with disciplined optimism – fundamentals and execution certainty remain central to underwriting.

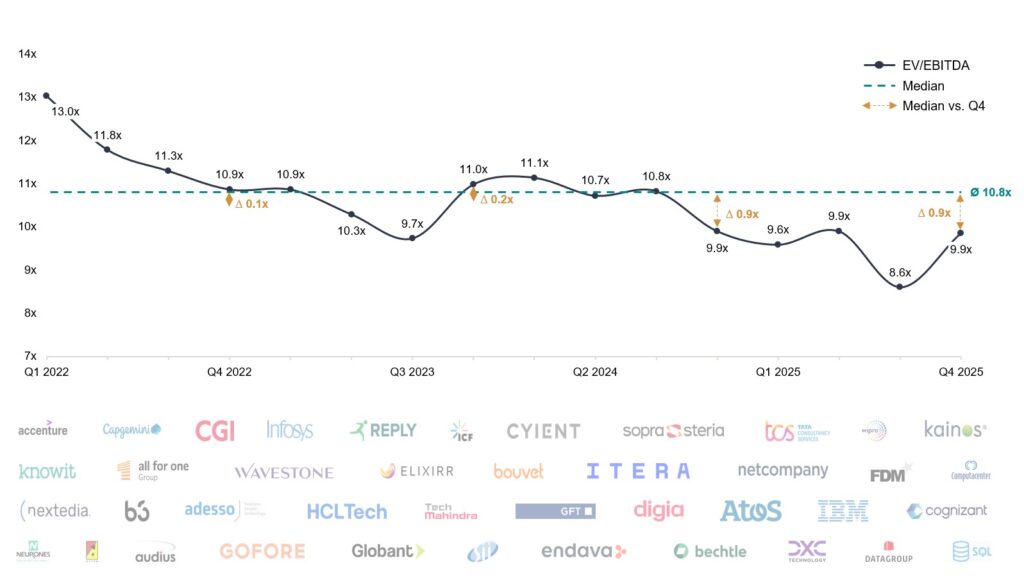

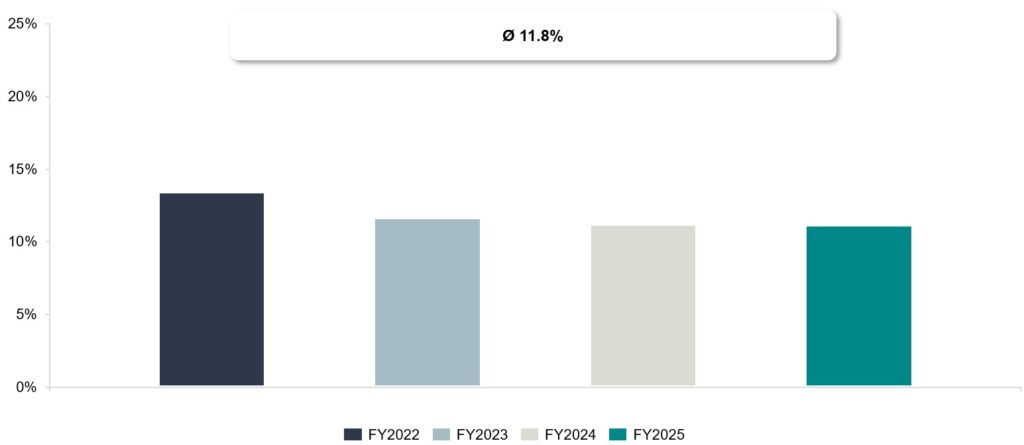

Valuation levels have stabilized, showing slight upward trend in Q4 2025

Convergence continues, as investors apply a uniform KPI lens, rewarding visibility and cash conversion. Valuations in Q4 25 vary between ~9-10x EV/EBITDA with an upward trend. Multiple upgrades require higher recurring mix and margin durability. Providers that productize delivery (templates, automation, near-/offshore leverage) tend to reduce volatility and sustain multiples better through cycles.

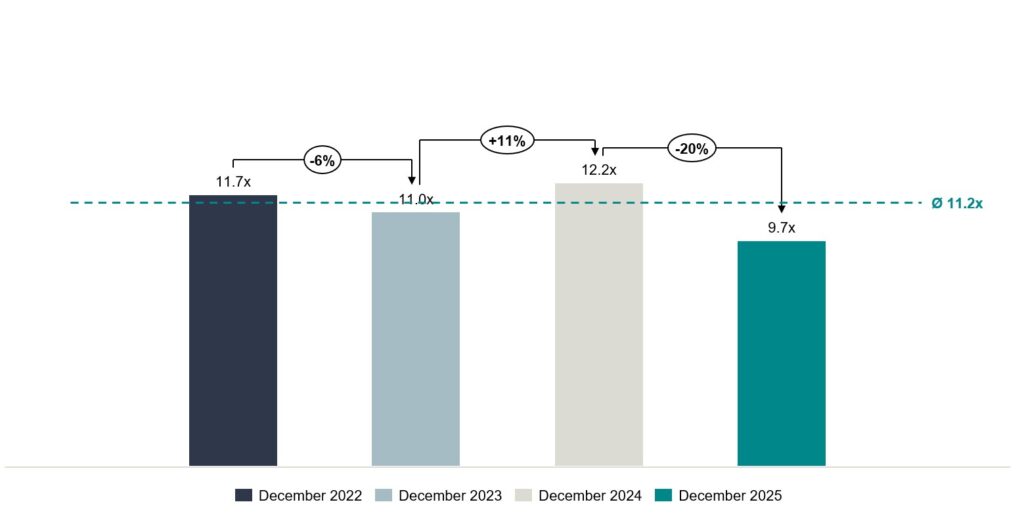

YoY EV/EBITDA valuation rebalancing: quality-first buying favours managed models over project-heavy delivery

YoY compression: Valuations declined as investors rotated to quality at tighter entry levels. The strongest pressure appeared in project-heavy models, where wage and bench frictions reduced margin visibility, while operate/managed models saw smaller drawdowns. With buyer discipline still elevated, the YoY reset aligns with the broader post‑2021 normalization in tech services multiples.

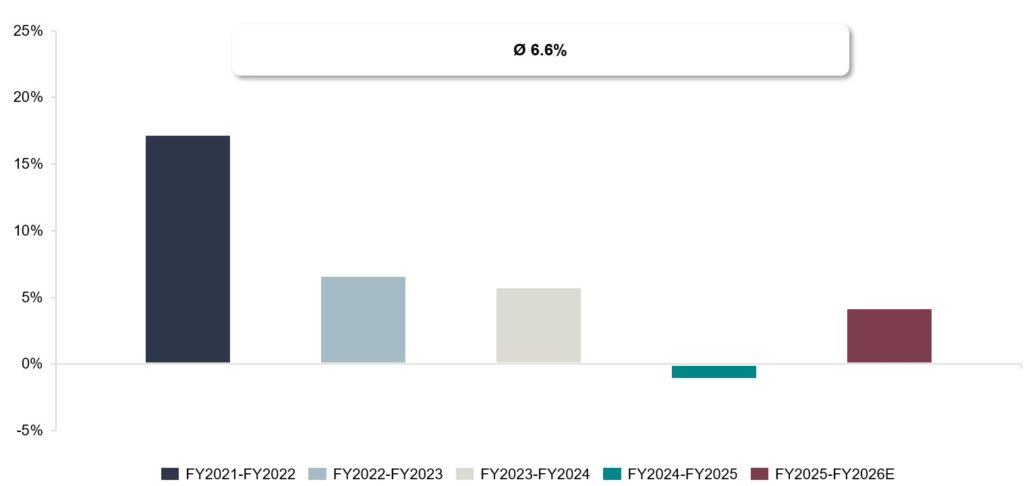

2026E revenue growth expected to resume as IT Spend re-accelerates and GenAI scales cloud delivery

2026E marks a rebound from a weak 2025 base. Two main forces drive the upswing:

- Budget re‑acceleration into IT Services (the largest IT spend category in 2026) and the restart of deferred programs

- GenAI-driven cloud demand: 2025 cloud infrastructure revenues reached $419bn (Q4 2025: $119.1bn), pulling through DataOps, MLOps, FinOps and security services into higher 2026 delivery.

EBITDA Margins stay resilient, best-in-class performance with key execution levers

Margins have shown only limited compression and remain structurally stable. Key aspects to watch:

- Where “best-in-class” sits: Scaled platforms tend to operate in the mid- to high-teens (e.g., Accenture 17.0% adjusted operating margin), while offshore-heavy leaders can reach the low-20s when mix and pricing hold (e.g., Infosys 21.1% operating margin).

- Key margin watch-outs: higher subcontractor mix, weak change control, stretched DSOs dilute margin quality and cash conversion

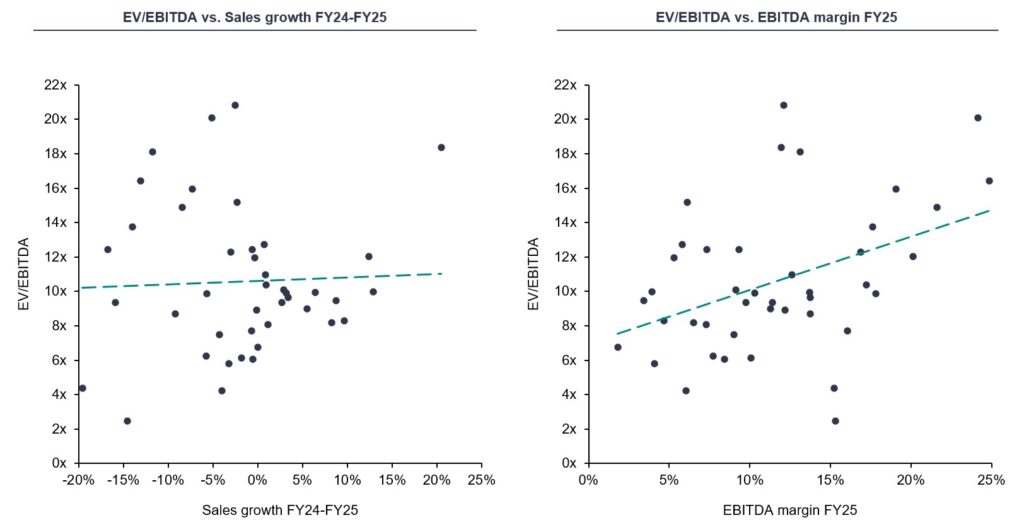

Investors reward profitable growth: margins, recurring revenue and cash conversion drive premium multiples

The market rewards profitable growth, not topline alone. Peers that combine solid margin with strong growth cluster at the upper end of sector multiples, while low‑margin growth screens as lower quality. Investors are looking for tight utilization, healthy gross margins and a rising recurring share – in other words, visibility, quality and cash conversion.

The Investec IT-Service Index tracks daily developments. The index includes valuations, growth projections, profitability margins and other metrics. You can find more information on our website.

Investec has a senior sector team in Technology, who are experienced experts in selling, buying, and financing businesses.

If you have questions and would like to know more about valuations, buyer activity and current opportunities in the market – please get in touch:

Ron Belt, Jean-Arthur Dattée, Thomas Ellenberger, Arne Laarveld, Matthias Odrobina , Sebastian Lawrence, Mirko Nikkels, Maurits Odekerken, Oliver Reinecker